A Strategy for Taxation of Retirement Assets after Loss of “Stretch”

By Matthew D. Blattmachr, CFP® Jonathan G. Blattmachr, JD, LLM, & Amber Gunn, CTFA

In some cases, it is beneficial for distributions from a qualified (pension) plan or an IRA to be paid over a rela- tively long period of time. One reason is that the longer assets are left inside such a plan or account, the more time they have to grow tax-deferred.

"After the changes to the Internal Revenue Code made by the SECURE Act, there is a substantially reduced time that the income taxation of assets in a plan or IRA can be postponed once the plan participant or IRA owner dies.”

After the changes to the Internal Revenue Code made by the SECURE Act, there is a substantially reduced time that the income taxation of assets in a plan or IRA can be postponed once the plan participant or IRA owner dies. (Special rules apply to what are called Roth IRAs which are not addressed in this article).

After the SECURE Act, long-term income tax deferral remains unchanged for select beneficiaries such as a surviving spouse, a minor child of the participant or owner, a disabled person, a person who is chronically ill, or someone who is not more than ten years younger than the participant or owner. All others, however, must take out the entire amount in the plan or IRA within ten years (or, in some cases, five years).

The options can be complicated when deciding the best way to continue to postpone taxation of interests in plans or IRAs; however, one strategy is to make use of a charitable remainder trust.

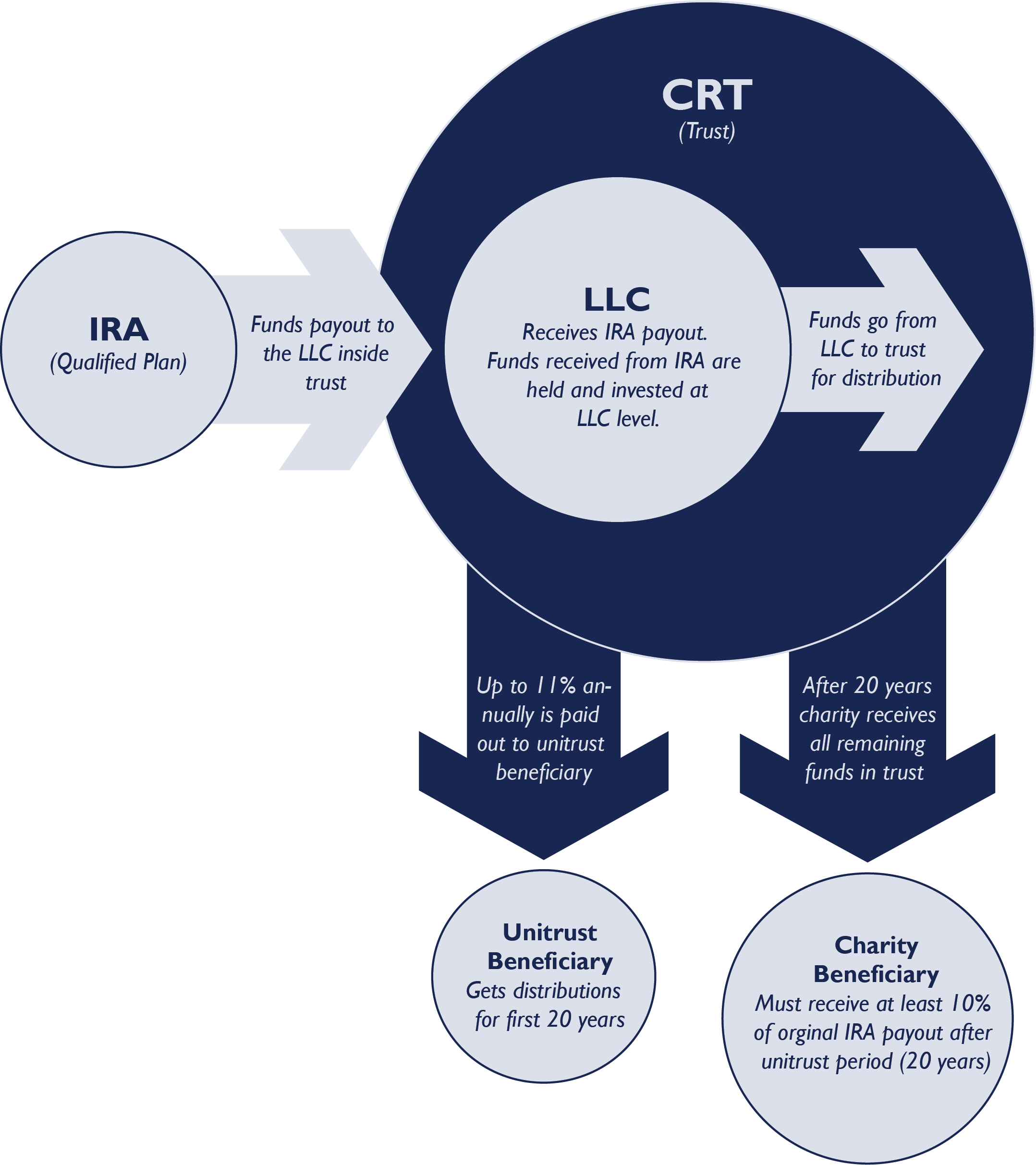

An Answer for Some: A Charitable Remainder Trust

A charitable remainder trust (CRT) is a trust where one or more individuals receive benefits for life or a fixed term (of not more than 20 years) and then the remaining property in the trust passes to charity. Both the Internal Revenue Code and regulations have detailed rules about CRTs. Generally, these trusts have been used to postpone taxation. For example, if a taxpayer decides to sell appreciated stock, the shares instead can be contributed to a CRT and the trust can then sell them without any tax because the trust is exempt from income tax.

Distributions from the trust are included in the recipient’s income under somewhat complex rules. Because a CRT is income tax-exempt, proceeds from a qualified plan or IRA can be paid to the trust when the participant or owner dies and no income tax will then be payable. However, as the plan or IRA proceeds are distributed out of the CRT, they will be taxed to the recipient.

A Special Kind of CRT: The NIMCRUT

The rules related to CRTs are complicated. One of the complications is choosing what kind of CRT to use. There are three types of CRT. One type, called a charitable remainder annuity trust (CRAT), pays a fixed amount (an annuity) each year to the beneficiary or beneficiaries. Actuarial rules limit how much of an annuity and for how long the CRAT can pay.

The second type, called a charitable remainder unitrust (CRUT), pays an annual amount equal to a fixed percentage of the annual value of the trust. If the trust grows in value, the beneficiaries receive more. If the trust declines in value, they will receive less. Actuarial rules also limit how much of a unitrust amount can be paid and for how long, but there is greater flexibility with a unitrust than with an annuity trust.

The third type is the most complicated but may offer the best results. It pays the lesser of either the unitrust amount or the “fiduciary accounting income” (“FAI” or simply “Trust Income”). This type of CRT is sometimes called a “Net Income” CRT. Trust Income is itself a complicated topic. Generally, it means income (as opposed to principal or corpus) under state law rules relating to trusts. Trust Income usually consists of dividends and interest and normally not capital gains, however, there are exceptions that a taxpayer may use to produce a better result.

With this third type, the law allows for amounts to be “made up” or paid in future years. For example, if Trust In- come is lower than the unitrust payment, the annual payment can be postponed until a year when Trust Income is greater than the unitrust amount. This type of CRT is sometimes called a “Net Income with Make-up Charitable Remainder Unitrust” or “NIMCRUT".

Why a NIMCRUT May Help with Plan and IRA Proceeds

Making plan or IRA proceeds payable at death to a CRT means they must be paid out within five years of the death of the participant or owner, however, there is no adverse income tax due to the CRT’s tax exemption. The CRT would invest the proceeds and, even if a NIMCRUT is used, Trust Income (such as a dividend or interest) would be earned and would have to be distributed to and taxed to the trust beneficiary, however, by “sandwiching” an entity, such as a limited liability company or LLC, between the CRT and the assets it invests in, Trust Income can be kept at zero. If and when it is desirable to generate Trust Income, the entity (that is, the LLC) can voluntarily make a distribution to the NIMCRUT which will then make distributions to the beneficiary for the unitrust amount for that year and for shortfalls in prior years.

As long as no Trust Income is generated (because the LLC makes no distributions), the value of the trust can grow entirely free of income tax. In fact, a NIMCRUT can provide for a yearly unitrust payment of 11% for 20 years. It will be noted that if the LLC (and thereby the trust) grows over time, the 11% will apply to ever-increasing amounts meaning more will be accruing for the beneficiary. If the LLC makes no distributions until the 20th year, no income tax will be due regardless of how much the LLC earns. If the beneficiary is under the age of 30, the payments can be made for the life of the beneficiary, but payments will usually be under 11% a year.

A limitation to keep in mind is that to have a valid CRT, the value of the remainder in the trust for charity must be at least 10% of the value of the assets when they are first transferred to the trust. That does not mean that the charity must receive 10% of what is in the trust when it ends. In fact, with the current low interest rates the IRS uses, the amount a charity receives at the end may be a very small percentage of what is in the trust when it ends.

Key Considerations for Drafting a CRT

The IRS has issued sample forms for CRTs which, if used, practically guarantees a valid CRT; however, these IRS forms can be modified to ensure a better result. It will almost always be best to have the value of the remainder when the CRT is created to be the minimum required, which is 10%. As indicated, the best benefit of a CRT is its exemption from income taxation. That exemption is available whether the remainder is 10% or greater. Since the family member of the participant or owner benefits from this exemption and loses the benefit to the extent the trust goes to charity, it usually is best to keep the charitable remainder value at 10% and not more. Those drafting a CRT may consider the included sample provisions to obtain this result.

Sample Language

Unitrust Amount. The Unitrust Amount shall be the lesser of: (i) the trust income for the taxable year (Trust Income), as defined in Internal Revenue Code Sec. 643(b) and the Regulations thereunder, and (ii) the “Unitrust Percentage Amount,” which shall be equal to the largest percentage, paid with the frequency provided below and using the highest rate published by the Internal Revenue Service pursuant to Internal Revenue Code Sec. 7520 that may be used to determine the value of the remainder of this trust under Internal Revenue Code Sec. 664(d)(2)(D), which percentage is not less than five percent (5%) and not greater than fifty percent (50%) of the net fair market value of the assets of the trust valued as of the first business day of each taxable year (the “valuation date”) rounded to the nearest one one-thousandths of one percent, paid for the term and at the manner specified above, such that the value of the remainder within the meaning of Internal Revenue Code Sec. 664(d)(2)(D) of this charitable remainder trust as of the date this trust commences shall be ten percent (10%) or, if it is not mathematically possible for the remainder to equal ten percent (10%), as mathematically close to but greater than ten percent (10%) as possible.

The LLC and Trust Income

In order to provide the greatest flexibility to produce as much or as little Trust Income as possible, the NIMCRUT should be funded with an LLC or similar entity. However, none of the trustees, the grantor of the trust, or any beneficiary of the trust can determine when distributions from the LLC may be made to the trust. However, some independent person, such as legal counsel to the grantor, can be given the power to control distributions from the LLC, by naming that person as a “non-member manager” of the LLC. That means that the person will have no ownership interest in the LLC and the LLC can be a “disregarded entity” for income tax purposes so its income will be attributed to the NIMCRUT, which being tax-exempt will owe no income tax on the income earned by the LLC. The included provision may be considered to obtain this result.

Sample Language

Limitation on Determination of Income.The determination of what is and is not Trust Income of this trust shall be made under Alaska law. In addition, the following rules shall apply: (1) proceeds from the sale or exchange of any assets contributed to the Charitable Remainder Trust herein created must be allocated to the principal and not to Trust Income, at least to the extent of the fair market value of those assets on the date of contribution, (2) proceeds of any sale or exchange of any asset purchased by the Charitable Remainder Trust herein created must be allocated to the principal and not to Trust Income, at least to the extent of the Trust’s purchase price of those assets, and (3) Trust Income may not be determined by reference to a fixed percentage of the annual fair market value of the trust property, notwithstanding any contrary provision and applicable state law.

Notwithstanding the foregoing, the following rules shall apply except to the extent but only to the extent that they depart fundamentally from traditional principles of income and principal within the meaning of Treas. Reg. 1.643(b)-1. The trust will not be deemed to have any Trust Income merely by the imputation of tax income to the trust from an entity, such as a limited liability company or a partnership, whether it is owed in whole or in part by the trust or of which the trust is a partner or member. Any cash distribution from such an entity shall be considered Trust Income except to the extent the entity advises the trust it constitutes a liquidating distribution.

Creating and Funding the Trust

It likely will be best if the NIMCRUT is created and funded with an entity, such as an LLC, prior to the death of the plan participant or IRA owner. The LLC (or other entity) may be named as the beneficiary of the plan or IRA. This way, the proceeds can be paid from the plan or IRA to the entity soon after the death of the participant or owner. The entire plan or IRA must be paid within five years of the death of the owner or participant.

Although the entity will be deemed to receive taxable income from the distributions, this income will be imputed to the NIMCRUT which is income tax exempt. In many cases, this may prove ultimately beneficial. For example, all distributions from a plan or IRA are taxed as ordinary income, but distributions from a CRT follow a more favorable tax regime. If capital gain income is earned in the plan or IRA after the death of the participant or owner, it will be treated and taxed as ordinary income. But, if the entity (LLC) receives qualified dividends, long-term capital gain or other income which is more favorably taxed than ordinary income, this better character or flavor of the income will be retained when and if paid out to the NIMCRUT beneficiary.

If you have more questions about Charitable Remainder Trusts & IRAs, get in touch with a trust officer at Peak Trust Company today!